Credit Card

Sin historial en EE.UU.: cómo empezar a construir crédito

Llegaste a este país con años de pagos responsables en tu nombre. Pagabas la renta,...

June 12, 2026

Llegaste a este país con años de pagos responsables en tu nombre. Pagabas la renta,...

June 12, 2026

El carro no arranca. O llegó una factura médica que...

Cada mes pasa lo mismo. Abres el estado de cuenta,...

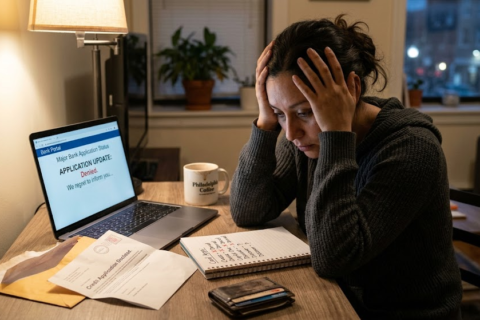

Llenaste la solicitud. Esperaste. Y después llegó el mensaje: solicitud...